The Chinese real estate sector is extremely important for both local and global macroeconomics, representing around 30% of China’s GDP (Gross Domestic Prod

The Chinese real estate sector is extremely important for both local and global macroeconomics, representing around 30% of China’s GDP (Gross Domestic Product). Just for you to have an idea: it’s an area that represents approximately one-third of the nation’s economic production.

The global market had high expectations for the economic reopening of China and the end of its “COVID Zero” policy. However, since these happened, the country’s economy hasn’t been growing at the expected pace.

In this article, we’re going to talk about the main aspects that have led the Chinese nation to its real estate sector crisis and what the possible effects are for global commodity chains. We’ve invited Alef Dias and Victor Arduin, Market Intelligence Analysts at hEDGEpoint Global Markets, to talk about this critical subject.

Continue reading and find out!

In 1998, China underwent a real estate reform, leading to a rapidly expanding market. Over the past 20 years, the real estate sector has benefited from ample credit facilities to continue to grow at an accelerated rate.

In addition, the influence of cultural factors can clearly be seen, since one of the prerequisites for the Chinese to get married has traditionally been associated with buying a house. Families have also purchased properties as a source of investment income.

However, easy access to credit increased real estate speculation and the sector’s indebtedness. The consequences? Many companies began to face financing and indebtedness problems, raising distrust among consumers and investors. Added to a challenging demographic structure, this resulted in several projects being paralyzed in 2022, a year marked by a 24% drop in real estate sales.

Alef Dias, Market Intelligence Analyst

“The Chinese real estate market presents the problem of corporate debt, which has been happening with more intensity since 2021. The government isn’t granting more stimulus, as it wants to avoid financial speculation,” Dias explains.

In December of 2022, the Chinese government abruptly ended its policy called “COVID Zero” which consisted of applying strict quarantine measures, together with mass testing of the population. The rules included strict lockdowns, with shops, schools, and businesses all closed.

Last year, China had one of its worst growth rates in four decades, according to official data. Health restrictions led many people to avoid leisure activities, which in turn reduced consumption. Many factories and businesses also had to shut down.

hEDGEpoint experts point out that the economic reopening of China, after the end of the “COVID Zero” policy, hasn’t generated the expected economic growth, and this is also directly related to the crisis in the country’s real estate sector:

Victor Arduin, Market Intelligence Analyst

“An intense reopening was expected, but that’s not what happened. The Chinese market hasn’t warmed up enough with the current fiscal and monetary incentives,” Victor Arduin remarked.

The whole world is slowing down economically due to very high-interest rates, which causes consequences such as an increase in credit for individuals and companies, compromising the pace of economic activities. Thus, it becomes more expensive to borrow money to buy goods and services, which can reduce production and demand, slowing down the entire economy.

Higher-than-expected inflation, particularly in the U.S. and major European economies, is tightening global financial conditions. As a measure to face this context and stimulate the domestic market, China lowered its interest rates.

“China has lowered its interest rates very little. This signals the government’s concern about not causing market jitters and price speculation, but it’s having a limited impact on boosting demand for housing and investment,” Arduin continued.

When there’s an economic slowdown in Europe and the U.S., as we’re currently seeing, the Chinese industrial sector may suffer more direct consequences than the real estate sector itself, which already faces its own problems. According to Arduin, this happens because European countries, for example, will be able to import fewer goods from China, if their population returns to consuming less.

“Without Europe’s imports, China will produce less, slowing down sales, and consequently, its overall economy,” the specialist clarifies.

The Chinese reopening hasn’t had the impact expected, especially when we talk about the demand for commodities. This can be largely explained by the fact that the recovery has been concentrated in the services sector.

China provides the main demand for several commodities in the world, mainly grains and energy. When an economic recovery is forecast, the expectation of greater demand for these commodities also exists, especially in the case of energy, since people tend to leave their houses more. The markets expected this, but it hasn’t happened.

In a scenario of greater economic activity, the stimulus to produce goods that require commodity imports for their development is present. Alef Dias explains the correlation here:

“The real estate sector hasn’t achieved the same performance when compared to services. A practical example: the construction industry itself needs more tractors. Tractors consume fuel, and if there were more construction and thus heating of the real estate sector, it would lead to a probable increase in the demand for oil, for example.”

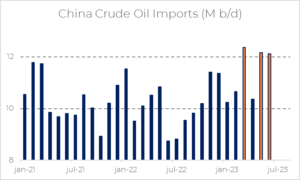

Victor Arduin points out that China’s slowdown in relation to demand for commodities is not homogeneous, as record oil imports were observed in March and May of this year.

“We’ve observed that the country has benefited from the war between Russia and Ukraine, taking advantage of Russian oil discounts, and improving the profit margin of its refined products,” Arduin adds.

Fonte: hEDGEpoint Global Markets

The prospect is for increased stimuli by the Chinese government. “We expect an increase in these incentives from the Chinese government, but it probably won’t be of the magnitude necessary to provide strong growth and compensate for all the slowdown we’re seeing in the West,” Alef comments.

hEDGEpoint analysis shows that the Chinese government is showing more favorability toward granting monetary stimuli. The problem is that interest rate cuts run the risk of being less efficient than fiscal stimulus, such as investments in new real estate sector projects.

According to analysts at Goldman Sachs, China is also likely to implement more easing measures in the second half which include:

However, the prospect is for a gradual and balanced recovery of the real estate market, avoiding overheating, as has happened in previous cycles.

hEDGEpoint continues to monitor all events that may affect the macroeconomy and have repercussions on commodity markets. Thus, we’re able to strategically offer risk management solutions to our clients.

Understanding all the factors that can impact commodities is vital to bring more security and protection to your business. Based on innovation, valuable insights, and market intelligence, hEDGEpoint provides essential hedging products to help you plan more effectively and make more assertive decisions.

Talk to a hEDGEpoint specialist today to learn more!

Rua Funchal, 418, 18º andar - Vila Olímpia São Paulo, SP, Brasil

Contato

(00) 99999-8888 example@mail.com

![]()

![]()