Corn and soybean crops play a strategic role in the global commodities market. South America has emerged as the main supplier of these crops, with Brazil a

Corn and soybean crops play a strategic role in the global commodities market. South America has emerged as the main supplier of these crops, with Brazil and Argentina among the world’s leading producers and suppliers. Production expectations for the 2024/2025 harvest in both countries combined are for new records, even in challenging weather conditions.

Expert Sol Arcidiácono, Grain Coordinator at Hedgepoint, was invited to discuss the soybean and corn crop scenario for 2025. Read on to find out the outlook, information on climate, production and prices, as well as the importance of hedging for South American producers. Happy reading!

Read also:

World soybean production is led by Brazil, with Argentina in third place in the ranking, although it is the main exporter of by-products, soybean meal and soybean oil. The production of both countries has a strong impact on international prices, influencing the entire production and commercial chain in the main consumer markets.

According to our expert, “Argentina mainly exports soybean meal and oil to Europe and India, respectively, while soybean exports are largely led by Brazil, with China as the main destination.”

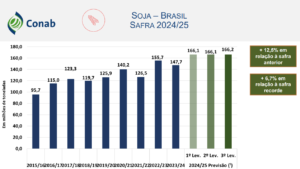

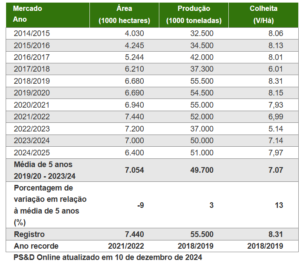

For 2024/2025, the Brazilian soybean harvest is expected to set a new record. According to the Conab (National Supply Company) report for December 2024, production is expected to reach 166.328 million tons, an increase of 12.6% on the previous harvest and 6.7% above the country’s all-time record.

Source: Conab

“In its January report, Conab slightly increased its projection for the 24/25 harvest, but these are conservative figures. The USDA is a little more optimistic and points to growth that will reach 169 million tons. Most private analysts are close to 170 million tons,” says Sol

The expert points out that the start of soybean planting in Brazil faced challenges this year due to the delay in the rains. However, the pace of planting recovered quickly and regular rains returned. Consistent rains in the center-north of the country contributed to increased productivity levels.

Read also:

In Argentina, USDA data corroborated the idea of increased productivity compared to the previous harvest, reporting that the country expects to reach 52 million metric tons (MMT) in 2024/2025. In the previous harvest, production was 48,210 MMT and the average for the last 5 years is 42,422 MMT.

However, Arcidiácono reports challenging obstacles affecting the soybean crop in Argentina in the last weeks of 2024 and early 2025. “The low level of rainfall could influence crop productivity. Initial moisture reserves were much better than last year, but the situation at the start of the year is worrying,” he says.

In January 2025, the Argentine Grain Exchange published graphs tracking the main productivity variables. Check them out:

Source: Bolsa de Cereales

“January is a decisive month for soybean development in Argentina. There has been an increase of 1 million hectares in the planted area, and the rains at the end of January and beginning of February should have a direct impact on the productivity of the crop. The 50 million tons that were a floor at the end of 2024 are now a target as of 2025,” concludes Sol.

Read also:

In Brazil, corn is advancing in its first harvest. The Conab survey indicates a slight reduction of 1.5% compared to the previous season. The figure published in January was 22.533 million tons, down from 22.962 in the previous harvest.

According to the USDA, Brazil’s first crop accounts for 24% of annual production. For the entire 2024/2025 season, the institution estimates that the volume harvested will be 127,000 MMT, an increase of 5 MMT on the previous year.

The Hedgepoint expert also points to an increase in Brazilian corn production. “We expect better corn production than initially expected, following the devaluation in Brazil, and growing domestic consumption. However, the definition is advanced, the winter crop is sown after the soybean harvest, which has a delay. In addition, the fall weather in the south defines yields, although the scenario is challenging because of the delay in sowing. The ideal rainy window could be missed when corn needs it most, and domestic use for fodder and ethanol is at record levels, around 90 million tons. Brazil’s 2025 exportable balance continues to be revised, but it will certainly be far from the 47 million tons estimated today by the USDA,” he says.

For Argentina, Sol points to expectations similar to those in Brazil. Corn production should also be maintained or increased in the final figures due to the good initial weather and the relevance of late or second crop corn, which would have a better window of productivity with good rains forecast for the end of January/February. The USDA estimates an adjusted increase of 1 million tons compared to the last harvest. See the data for the last 10 years:

Source: USDA

The Bolsa de Cereales Argentina reports good weather conditions for this harvest. At the beginning of January, 93% of the water conditions were considered optimal or adequate for the crop, while at the end of the month this indicator stood at 59%. “The crop suffered a lot in January, but we still have room to defend it. Margins would improve considerably, especially with the recent reduction in retentions, although the recent measure favors soybeans more,” says Arcidiácono

Read also:

In addition to production estimates, expert Sol Arcidiácono also addressed issues that impact the competitiveness of Argentine and Brazilian products in the commodities market. The macroeconomics of each country, as well as the expansion of supply, are some of the main factors influencing prices for 2025.

Soybean values will suffer the impact of the Brazilian surplus crop and increased volatility. The market will be challenging for producers, requiring greater attention to market opportunities,” she says

Sol also points out that changes in the purchasing power of the Brazilian real and the Argentine peso have an impact on products. The Brazilian currency lost value last year, increasing the competitiveness of this origin on the world market. Argentina’s currency has appreciated, reducing opportunities for its commodities. The government’s adjustment of export taxes on grains and by-products was a logical step.

Read also:

“Soy exports in Argentina lose out because they face higher taxes. Climate risk in the country also affects price volatility,” adds the Hedgepoint coordinator. According to the expert, adverse weather in Argentina creates early sales opportunities for local producers. It’s important to monitor the market and act strategically.

“Normally, producers expect better prices in the future, but this year is not ideal. We have to be attentive to weather conditions and volatility to avoid big losses, the margin is clearly at risk,” adds Arcidiácono.

These changes in climate and currency exchange rates are variables that increase the financial risk for producers and companies. In this scenario, hedging is a necessary tool to mitigate this problem and protect market players.

Hedgepoint has specialists in corn and soybean hedging in South America, ready to meet the needs of each client. Get in touch and count on financial risk management and a complete team!

—————————————————–

Rua Funchal, 418, 18º andar - Vila Olímpia São Paulo, SP, Brasil

Contato

(00) 99999-8888 example@mail.com

![]()

![]()