2024 in Review: A Year of Volatility and Challenges in the Commodities Market

Commodities in Review 2024 for soft commodities, grains, energy and macroeconomics.

2024 brought significant challenges to the commodities market, influenced by a dynamic macroeconomic scenario and significant climate events. Persistent inflation in the United States strengthened the dollar, while changes in ECB (European Central Bank) monetary policy and the fallout from the U.S. election added volatility to the global outlook.

In agricultural commodities, adverse weather conditions impacted sugar, coffee and cocoa, with severe droughts and high costs depressing production in key regions. On the other hand, cereals faced a more favorable scenario with a recovery in Argentina and high productivity in the USA, although dry weather in Brazil posed new challenges.

The energy sector also experienced ups and downs: geopolitical tensions boosted oil prices, but weakening global demand signaled a bearish outlook for next year.

This macro review reflects the key factors that shaped prices and supply in the commodities market, highlighting the complexity and interdependence of these markets in a year full of challenges and uncertainties.

In this article, Hedgepoint provides a comprehensive analysis of the key developments in the commodities sector. Read the text and see all the highlights highlighted by our experts.

Macroeconomics in 2024

After a start to the year marked by persistent inflation in the U.S., inflationary pressures began to ease, allowing the Federal Reserve (Fed) to begin lowering interest rates in September with a 50 basis point cut. Prior to this, the European Central Bank (ECB) had already begun its monetary easing in April, resulting in a depreciation of the euro against the dollar.

Even with the Fed’s interest rate cuts from September, the dollar remained strong, supported by the uncertainties surrounding the U.S. elections. In November, the confirmation of Trump’s victory reinforced these expectations and kept the dollar at high levels.

Donald Trump’s victory led to speculation of an inflationary economic agenda, with possible tax cuts and protectionist trade policies. Meanwhile, the ECB loosened its monetary policy, improving the economic outlook for the region but weakening the euro against the dollar, which remains strong due to the longer-term maintenance of higher interest rates.

This macroeconomic context has highlighted the complexity of balancing economic stimulus and exchange rate stability in a global environment of uncertainty. See data collected throughout the year on the US Dollar Index (DXY) and the JP Morgan Emerging Markets Currency Index (USD):

Sources: Refinitiv, Hedgepoint

Read also:

- Understanding the Federal Reserve’s (FED) Impact on the Brazilian Economy

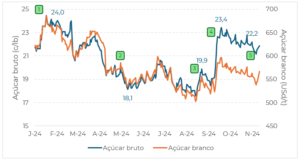

Weather and the Sugar Market in 2024: Challenges and Forecasts

The weather was the main protagonist in the sugar market in 2024. The drought and fires in the Center-South (CS) of Brazil supported prices, while the recovery of crops in the Northern Hemisphere (NH) limited the increase. Brazilian production is expected to decline in 24/25 after a record 23/24.

The good start to the 24/25 crushing season in the CS, favored by low rainfall, eased supply and put downward pressure on prices. However, the persistence of the drought and the trade flows expected in late 2024 and early 2025 supported prices. However, the persistence of the drought and the trade deficit expected for late 2024 and early 2025 supported prices. The difference between the expected availability of raw sugar and white sugar put pressure on the white sugar premium.

The rains in the CS have started to benefit the 25/26 crop, while regions such as Europe, Thailand and Central America indicate higher future supply. In addition, weak demand has put pressure on sugar prices, which find some support from supply constraints in the Brazilian off-season.

Sources: Refinitiv, Hedgepoint

See also:

- Development of the bioenergy market in Asia

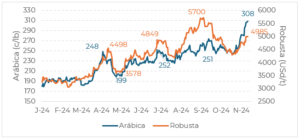

Coffee in 2024: a year of highs and volatility

Adverse weather conditions made the year challenging for the coffee market, with supply constraints and below-average stocks in several producing and consuming countries. Production declines in Brazil and Vietnam were the main drivers of tight supply and price volatility.

In Vietnam, reduced production in 23/24 resulted in lower stocks, with farmers reluctant to sell even at higher prices. Hot and dry weather conditions in early 2024 increased risks for the 24/25 crop, putting pressure on Robusta prices and consequently on Arabica. In Asia, Robusta shortages in Vietnam hampered trade.

Coffee prices rose again in November, driven by storms in Central America and concerns about a small 25/26 Arabica crop in Brazil. This scenario pushed Arabica futures to new records, while Robusta prices also rose significantly.

Sources: Refinitiv, Hedgepoint

Grain Market: Money, Climate and Geopolitical Uncertainties

The year was marked by macroeconomic and climatic factors that shaped the grain market. Funds remained short throughout the year, reflecting bearish sentiment driven by robust harvests in the US and Argentina and favorable weather conditions in Brazil.

The war in the Black Sea also affected the sector, with Russian attacks damaging strategic ports and disrupting grain trade in the region. In Argentina, soybean yields returned to normal levels after the drought of 2023, while problems such as the Chicharrita pest reduced corn estimates.

In China, strategic buying on the spot market pressured prices as the country sought to diversify its sources ahead of Donald Trump’s inauguration. Trump’s re-election brought uncertainty about the trade war, with the strengthening of the dollar and the increase in Chinese inventories reducing U.S. exports and depressing prices on CBOT.

Despite good harvests in the Southern Hemisphere, dry weather in Brazil delayed soybean planting and threatened corn in the U.S. Late year rains helped improve planting conditions in Brazil and Argentina and supported U.S. logistics, but the political and geopolitical environment still added volatility to prices.

Sources: Refinitiv, Hedgepoint

Vegetable Oils in 2024: China, Margins and a Strong Dollar

The vegetable oil market was impacted by global economic and political dynamics, particularly in China, reduced crush margins and a strengthening dollar. Rumors of a delay in the EUDR also affected the market throughout the year.

A strong US dollar played a key role in the final months of the year, making soybean oil more competitive against palm oil. However, low production numbers and high local prices in China boosted palm oil futures. Fund activity, particularly in soybean oil, supported prices, while mid-year profit taking pressured palm oil values.

As crush margins recovered in China, economic activity picked up, supporting the market. Supply constraints in Thailand and increased imports from India contributed to a recovery in palm oil. Policy decisions by the Trump administration, particularly on tariffs, are eagerly awaited and could further alter the balance of vegetable oils.

Sources: Refinitiv, Hedgepoint

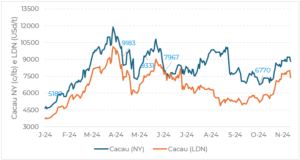

Cocoa Production: Challenges and Recovery Prospects

Global cocoa production faced significant challenges in 23/24, with Ivory Coast and Ghana recording below-average volumes due to extreme weather conditions, high production costs and economic crises. Although a recovery is expected in 24/25, volumes are still expected to be below expectations, particularly in Ghana.

In early 2024, prices began to respond to tighter global supplies, but the market still expected demand to decline due to higher prices. Both the Cocoa Association of Asia and the Cocoa Association of Europe reported a decline in crushing at the end of last year. However, with weather challenges in key producing regions, cocoa set successive records in the first and early second half of the year.

Despite optimistic forecasts, such as an increase in Ivory Coast production to 2 million tonnes in 24/25, the global equity index fell to its lowest level in 50 years as the market remained wary of the climatic and phytosanitary impact on the upcoming crop.

Sources: Refinitiv, Hedgepoint

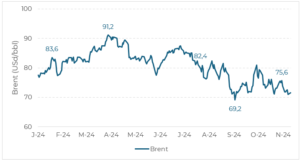

Geopolitics and oil: the highlights of 2024

The geopolitical scenario defined the direction of the energy market in 2024. Conflicts such as that between Israel and Hamas and the war between Ukraine and Russia boosted oil prices, while weakening global demand, particularly in China, led to a bearish outlook for 2025.

The year began with prices supported by low temperatures in the US, which disrupted production and refinery operations. In April, attacks related to the conflict between Israel and Hamas, including direct tensions with Iran, increased risk premiums.

From August onwards, signs of weakening demand, in particular a fall in China’s oil imports, added to market concerns. Donald Trump’s victory in the US elections in November is expected to boost fossil fuel production and increase domestic production.

Nevertheless, rising global supply combined with weaker Asian demand led to a more bearish tone for energy commodities towards the end of the year, setting the market up for a transition in 2025.

Sources: Refinitiv, Hedgepoint

See also:

- IEA energy outlook for Southeast Asia

Follow other reports on the Hedgepoint HUB

Access other complete commodity market reports directly on the Hedgepoint HUB. Experts discuss data on supply, demand, weather forecasts, acreage and more. Check it out now!