Coffee in South America: Crop Expectations for Brazil and Colombia

Learn about expectations for the South American coffee crop with Laleska Moda, Market Intelligence Analyst at Hedgepoint.

Brazil and Colombia are the two biggest coffee producers in South America. According to Embrapa, this continent contributes 46% of the world’s coffee production, of which Brazil accounts for 76% and Colombia for 17%.

In this article, we will examine the importance of these two countries for the global coffee market, expectations regarding exports, prices, yields, and other factors. For this, we count on the expertise of Laleska Moda, Market Intelligence Analyst at Hedgepoint, and Victor Sousa, Coffee Relationship Manager, who provide insights into the 2024/2025 crop. Enjoy reading!

South American Coffee Production Estimates

South America is a key region for coffee production, favored by ideal climatic conditions. Colombia stands out as the world’s largest supplier of washed Arabica, while Brazil leads the world in both coffee production and exports.

In Brazil, the 2024/2025 harvest was completed in August. In Colombia, the main harvest is expected to begin this month and continue until early 2025, while the Mitaca harvest was completed in August. See the full calendar below:

Source: Hedgepoint

Read also:

- Crop Calendar: Planting and Harvesting Times for the World’s Major Commodities

As major producers, the coffee crops in Brazil and Colombia play a key role in the global supply. However, recent seasons have seen production problems around the world, particularly in Brazil and Vietnam. These recurring crop shortfalls have impacted market prices.

“In this Brazilian crop, we have seen that the beans were smaller than expected at the beginning of the year. The initial estimate for Arabica and Robusta production was 65 million bags, but the final figure was adjusted to 63 million,” says Laleska.

“In this Brazilian crop, we have seen that the beans were smaller than expected at the beginning of the year. The initial estimate for Arabica and Robusta production was 65 million bags, but the final figure was adjusted to 63 million,” says Laleska.

Brazilian Robusta coffee (Conilon) saw a significant drop from 22 million to 20 million bags harvested. Meanwhile, Arabica production, originally estimated at 44 million bags, was slightly adjusted to 43.2 million.

“The drought in Brazil had a negative impact on the national crop. In Colombia, on the other hand, the weather has been more favorable and could contribute to a recovery in local production,” adds Laleska.

According to Victor de Sousa, the Colombian coffee market is expected to increase production this year due to the recovery in rainfall. “With two annual harvests, Colombia stands out from other countries and could see a slight increase in production, reaching 12.4 million bags, or 7.2% of world production,” he affirms.

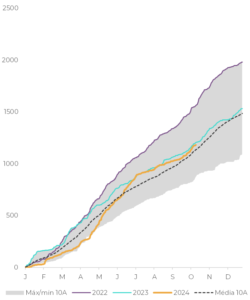

See data on Colombia’s good rainfall index below:

Cumulative Rainfall – Colombia (mm)

Source: Refinitv

Read also:

- Brazil’s role in China’s food security: a 50-year partnership

Expectations for coffee exports and destocking

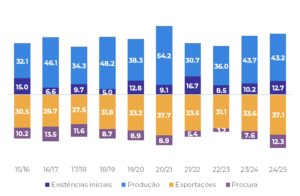

Hedgepoint’s research indicates an increase in Brazilian coffee exports for both Arabica and Robusta. Below we analyze the estimates:

Supply and Demand – Arabica – Brazil (M bags)

Source: Hedgepoint

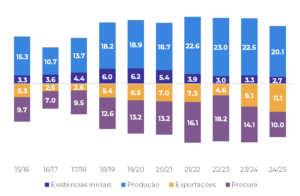

Supply and Demand – Conilon/robusta – Brazil (M bags)

Source: Hedgepoint

As can be seen from the charts, the production of Arabica coffee in Brazil remained practically stable, while Robusta experienced a more pronounced decline. The reduction in supply and the collapse in Vietnam in 23/24 have increased the price of this type of coffee on the market, encouraging farmers to opt for exports and take advantage of this increase in value.

“Conilon is highly valued in Brazil and this could contribute to cumulative exports in the 24/25 season increasing by more than 2 million bags compared to 23/24.

However, we estimate that global demand for Robusta could be lower this season,” adds Moda.

For Colombia, the Hedgepoint specialist expects an increase in the share of Arabica coffee exports due to production growth. However

Demand for Colombian coffee may remain weaker than in previous years, given the higher value of washed Arabica on the global market,” concludes Moda.

Read also:

- Understand the importance of logistics in agribusiness

Estimates of coffee prices in South America

According to Moda, the shrinking supply has increased coffee prices in the commodity market. “What we can see for the coming months is a price correction due to the rains forecast for Brazil and the possible advancement of the EUDR.

However, the dry weather that has affected the country so far is also influencing future values. The 25/26 harvest is currently in flower and has suffered from the lack of rain in the region,” says Sousa.

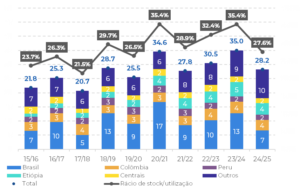

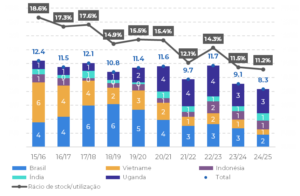

According to the expert, another factor supporting the high price of coffee in the long term is the reduced stock. “Overall, global stocks will remain at levels below historical averages.” Check out the data below:

Origins – Ending stocks of Arabica and stock/use ratio (M bags)

Source: Hedgepoint

Origins – Final stocks of Robusta and stock/use ratio (M bags

Source: Hedgepoint

According to the International Coffee Organization, prices have already been rising in recent months. Green coffee, for example, rose 1% in August 2024 compared to the previous month. Colombian mild coffee rose 2.3% over the same period.

Also read:

Global outlook and traceability of the coffee market

The European Union’s proposal to postpone the implementation of the regulation on deforestation (EUDR) until December 2025 has brought temporary relief to coffee producers, who are struggling to adapt to the strict requirements.

“This possible postponement will allow coffee exporting countries, such as Brazil, to adapt their traceability systems and sustainable practices. It is worth remembering that many European importers have brought forward their purchases due to the EUDR and with the possible postponement, buying pressure may decrease in the short term, putting downward pressure on prices. On the other hand, the postponement is seen as positive for Brazilian exporters, who will have more time to adapt to the new rules,” Sousa said.

Countries like Brazil and Colombia are ahead in the adaptation process, with a significant portion of their farmland already meeting sustainability standards. However, smaller countries or those with less infrastructure, such as those in Central America and Africa, face enormous challenges in ensuring compliance with the new rules, especially in areas where coffee production is linked to deforestation.

“In addition to the European Union, other regions such as the United States are likely to adopt similar regulations focused on sustainability and traceability in the coming years. This will increase pressure on coffee producers around the world to adapt to stricter standards and promote more sustainable agricultural practices,” concludes Sousa.

Commodity Reports on Hedgepoint HUB

Access comprehensive reports on agricultural and energy commodities on the Hedgepoint HUB portal. There, other experts analyze market data in depth and regularly publish information on supply, demand, weather, prices and more.

Visit Hedgepoint HUB to learn how we can help your business.