Brazil: leading player in the sugar market in 2024?

Brazil will play a leading role in the sugar market in 2024. Estimates are promising: record production is expected for the 23/24 season and good figures for 24/25 as well.

With a delicate global scenario, mainly due to the situation in India, the Brazilian nation has the potential to balance supply and demand at a global level. The country will therefore be key in influencing sugar prices.

Aspects such as the weather, macroeconomics and geopolitical conflicts also influence the sugar market, intensifying volatility. In this context, it is essential to adopt hedging tools capable of managing risks.

Follow our exclusive content and understand how Brazil can be a key player in this market in 2024. Happy reading!

Understanding the balance between global supply and demand in the sugar market

Currently, trade flows remain tight in the sugar market, considering the window between the first quarter of 2024 and the first quarter of 2025. In other words, we’re looking at the 23/24 cycle and the start of the 24/25 cycle.

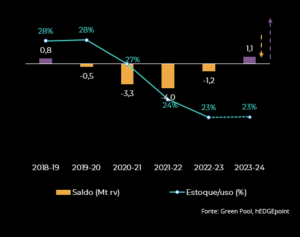

In terms of the global balance, the 23/24 harvest from October to September should be in surplus, a direct reflection of the Brazilian record. On the other hand, with the deterioration of growing conditions in the Center-South, a deficit is currently expected.

In this case, any worsening of the already tight availability conditions could trigger price increases. While the situation has not been so favorable for Brazil, the results expected for the country are still at the upper limit of recent years. However, when compared to the 23/24 season, the 24/25 harvest represents a significant reduction.

As far as the Northern Hemisphere is concerned, the climate is expected to be more favorable for sugarcane development, especially if La Niña is not so intense. In this scenario, the phenomenon would cooperate with the monsoon regime.

As a result, producing countries in Southeast Asia, such as India and Thailand, may have greater availability. In the case of the former, this will not necessarily lead to exports, as they will be dependent on three issues:

● Surplus volume after a resumption of the ethanol program.

● Price environment.

● Government measures.

At the current crushing rate, Thailand could reach a production of 8.5 million tons of sugar in 23/24. As for the 24/25 season, given the favorable weather conditions, it won’t be surprising if the country reaches around 10 million tons of sugar. If these figures are confirmed, there could be an increase in exports.

Global sugar balance (mt rv-outset)

What are the prospects for sugar production in Brazil this year?

Brazil had its biggest harvest in 23/24, with record sugar cane numbers and is expected to crush 655 million tons by . In November, December and early January, production was excellent, with figures higher than usual for the fortnight.

In this sense, the country is able to meet international market demand at a time of tighter supply in the Northern Hemisphere. The Center-South region was extremely important for the current season’s figures, with favorable weather conditions that contributed to cane productivity and crushing.

However, for 24/25, the weather brings the greatest volatility to the sugar market. Its impact remains the most significant risk factor for the 24/25 harvest in Brazil and could contribute positively to the bullish outlook.

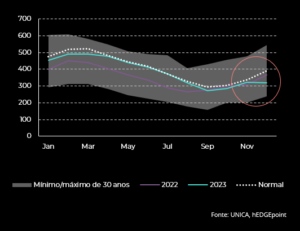

February’s rainfall and humidity, coupled with the unfavorable weather in the first half of March, dampened optimism about sugarcane volume projections. The northern part of the region was significantly more affected than the south.

Therefore, estimating the real impact of the drought remains difficult and allows us to point to a sugarcane production of 605.8 million tons. Of this figure, 41.75 million tons would be destined for sugar production.

Average soil moisture in CS (mm in top 0-1.6 m soil)

The reduction in productivity could reach 8.4%, which translates into an average TCH (tons of cane per hectare) of almost 79 t/ha. In this way, the recent drought in the Center-South and the reduction in yields could lead to a bullish factor in prices. On the other hand, an improved harvest in the Northern Hemisphere could boost the bearish factor.

Sugar market: what are the main risk factors in 2024?

There are three main factors that can accentuate volatility in the sugar market. Below, we explain each of them.

● Weather

It’s important to bear in mind that sugar production depends considerably on climatic conditions. The year 2024 brings the risk of a change from El Niño to La Niña, with the possibility of this climatic event starting in July.

The upward or downward trend will depend on the intensity of the phenomenon. If it’s more subtle, it could contribute to a higher concentration of sucrose in Brazil and cause above-average rainfall in the Northern Hemisphere. Both situations are positive for availability and bearish for price.

If there are frosts in Brazil and floods in the Northern Hemisphere, there is a chance of problems for the sugar market, due to negative impacts on production.

Read more: The influence of climatic phenomena on the commodities market

● Conflict in the Red Sea

Although the current conflicts do not affect the main sugar producers, there is a chance of repercussions, especially through the energy complex.

The ongoing conflict in the Red Sea is causing interruptions and increased costs in international trade with East Africa and East Asia. It therefore poses the risk of reducing an already scarce supply, which is causing a squeeze on various markets that depend on ships passing through this region.

● Macroeconomics

Central banks around the world are likely to start cutting interest rates. This scenario contributes to a bullish outlook. However, the increase in debt could slow down the process. It will therefore be essential to monitor macroeconomic movements.

Read here:

Hedgepoint: risk management in the sugar market

The sugar market is volatile. After all, it depends significantly on the weather and geopolitical and macroeconomic issues.

Producers and other players in this sector therefore need instruments capable of managing risks in order to protect themselves from price fluctuations. Commodity hedging exists precisely for this purpose.

In this way, you can guarantee a fixed amount of buying and selling to protect yourself from market rises. This is the case with agricultural derivatives, for example. At Hedgepoint, you have access to hedging tools and market intelligence analysis from our team.

In this sense, we follow all the events that can cause changes in the dynamics of commodities. With Hedgepoint HUB, our educational platform, we offer detailed courses and reports to train individuals with different levels of knowledge.

Access the Hedgepoint HUB now, get a 1-month free trial and start preparing to manage risks in the sugar market.