Wheat harvest in Argentina: understand the current scenario

See how the wheat harvest in Argentina is closing. What are the prospects for the commodity in the country.

The wheat harvest in Argentina for 23/24 arouses the attention of the world market, since the country is an important exporter of this commodity.

Difficulties have marked the current wheat season. Despite the rains in the last stage, favored by the arrival of El Niño, it has not been possible to compensate for the previous problems, among which the presence of frosts and droughts throughout the crop cycle in the producing regions of the country stand out.

This scenario is compounded by global events that have an impact on wheat supply and demand around the world. With this in mind, we invited Sol Arcidiácono, Head of Grains of hEDGEpoint’s Latin American Division, to talk about this topic.

Read on and find out more!

Wheat market: what is the relationship between world supply and demand?

Currently, the wheat market is attentive to three main axes:

- The trade balance of the 23/24 cycle in the northern hemisphere.

- The final phase of wheat definition and harvest in the southern hemisphere for 23/24.

- Crop development for the 24/25 cycle in the United States and Europe.

Sol Arcidiácono, Head of Grains of hEDGEpoint’s Latin American Division

In the context of the world wheat market, the huge harvest in Russia compensated the lower export flow from Ukraine and mainly defines the international price ranges. In North America, U.S. production was somewhat higher than expected, despite the severe drought in Kansas, while Canada maintained a good level of exports.

“The end of the year is a time of transition cycles. The main focus will always be outside the Americas. We must remember that 48% of world exports are concentrated between Europe and the Black Sea, a fundamental detail in the wheat market,” Arcidiácono explains.

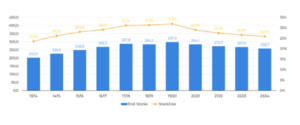

The evolution between world supply and consumption shows that wheat ending stocks are tight. Wheat prices, on the other hand, show a negative performance in 2023.

“The stock situation is less comfortable. Despite this, speculators have increased the wheat selling position in the Chicago market throughout the year. Supply pressure from Russia, primarily, has been felt strongly in the market this northern fall,” Arcidiácono notes.

Evolution of world ending stocks (million tons)

Source: USDA

Wheat Reference Prices – Major International Exchanges

Source: Refinitiv

For the southern hemisphere, crop prospects are challenging, even if the supply available in the northern hemisphere eases tensions.

Read also:

- The law of supply and demand and price formation

Below, we explain in detail the wheat crop situation in Argentina.

See how the Argentine wheat harvest is progressing

Today, the factors that define the wheat market in the southern hemisphere include aspects such as harvest, regular crop condition and weather challenges. According to the Rosario Stock Exchange (BCR), the wheat crop estimate for the 23/24 cycle totals 14.5 million tons, against 11.5 million tons last season. However, the result indicates the second worst harvest in the last 8 years.

The drought that affected part of the productive areas of Argentina, accompanied by late frosts and the effects of fungal diseases after the rains, explain this figure. In a suitable climatic context, the harvest could reach up to 17 million tons. In addition, BCR data consider a sown area of 5.5 million hectares, with an area loss of 390 thousand hectares.

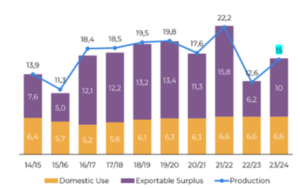

Wheat supply and demand in Argentina (million metric tons)

Source: USDA

With a harvest progress of approximately 70% at the end of the year, the progress of the harvest in the province of Buenos Aires substantially improved the final result. The wheat-growing region par excellence contributed to the cause, mitigating the climatic impact on yields, as conditions were much more favorable.

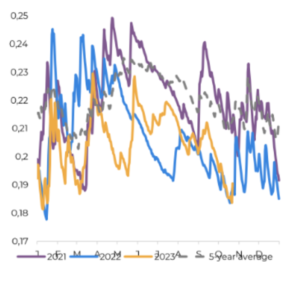

Rainfall anomalies – September 23 (mm/day with respect to normal)

Source: hEDGEpont, NOAA

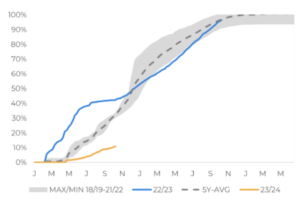

Soil moisture has been very low in the Center-North region. Therefore, the scenario is extreme, with minimum levels, as in the previous cycle, as shown in the following graph.

Soil Moisture – Argentina (% in the first meter)

Source: Refinitiv

- Read here: The influence of climatic phenomena on the commodities market.

Exports: see which countries have the highest demand

In the international market, sales of Argentine producers in the cycle that closed have been extremely low, only around 3 million tons of wheat from the 22/23 harvest have been shipped, in a year where the commercial flow was also influenced by the possibility of a change of administration, since the transcendent presidential elections took place in the middle of the definition stage and the advance of wheat harvesting.

Evolution of farmers’ sales in Argentina (% of production)

Source: Ministério de Economia da Argentina

Regarding the external demand for wheat, Sol Arcidiácono stresses the importance of observing the following factors:

- The increase in domestic prices in the Indian market, a sign of possible measures to enable imports, considering the adjusted level of inventories.

- China will be a relevant importer due to lower production and quality problems of domestic wheat. It has surprised by buying more than 2 M tns of wheat from the United States recently.

- Demand from North Africa is robust.

- Doubts surround Brazil, as important states such as Rio Grande do Sul and Paraná had their wheat production affected by excessive rains.

“It was the spring that recorded more rainfall in southern Brazil, which affected the quantity, yield and quality of wheat harvested in the region,” notes the Head of Grains of hEDGEpoint’s Latin American Division.

In this scenario, Brazil should maintain stable exports, diversifying imports. This is due to the worsening quality of the crop in the south of the country and the decline in Argentine wheat production.

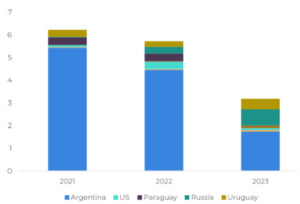

Origins of Brazilian imports (million tons)

Source: Comex

hEDGEpoint: risk management for the wheat market

As we have seen, Argentina has been recovering from one of the worst wheat cycles in its history, but it is still at levels that are considered low. In this sense, the country also experienced an election year and unfavorable weather for the commodity’s producers, factors that together accentuate volatility.

Given this reality, risk management is an important ally for producers and other participants in this market. With sophisticated hedging products, it is possible to apply tools that contribute to strategic decision making, such as the use of agricultural derivatives.

hEDGEpoint works to provide hedging instruments combined with market intelligence and in-depth analysis. In this way, we monitor all movements that can affect the wheat market both locally and globally.

Contact a hEDGEpoint professional and see how we can manage risk in your business.